Why the CISO Belongs in the Cyber Insurance Process

Cyber insurance transfers financial risk effectively only when the coverage reflects the organization's financial risk. The CISO sits at the intersection of risk measurement and risk communication. This article covers how that position makes the CISO essential to the insurance process, and how quantifying cyber risk aligns coverage decisions with the organization's actual exposure and risk appetite.

- The CISO's visibility into controls performance, threat scenarios, and residual risk gives decision makers the inputs they need to assess coverage accurately.

- FAIR-based scenario modeling produces financial outputs that map directly to policy structure, making coverage adequacy analytically testable rather than assumption-based.

- Cyber risk presented in financial terms gives CFOs, boards, and brokers the data they need to make defensible decisions about risk transfer, retention, and coverage levels.

What the CISO Brings to the Insurance Conversation

Quantified Analysis that Drives Coverage Decisions

In many organizations, the CISO is brought into the cyber insurance process only to complete the technical section of an underwriting application. This significantly undervalues their role.

Underwriters assess loss event frequency and loss magnitude to set rates and determine policy terms. A CISO who has integrated quantitative methods like FAIR into their risk management process evaluates cyber risk the same way. The FAIR methodology models cyber risk as loss event frequency and loss magnitude expressed as calibrated financial ranges. This mirrors the framework underwriters use to price and write a policy.

Underwriting scrutiny varies by organization size and sector. Larger organizations and those in high-risk industries often face detailed documentation requests, control verification, and in some cases on-site audits. Smaller organizations may encounter a questionnaire-based process. In both cases, underwriters are evaluating the same underlying questions about frequency and magnitude, which makes the CISO a natural contributor to the insurance conversation.

Reading Policy Language Against Real Scenarios

A cyber insurance policy covers losses by loss type, and each type carries its own sublimit and retention threshold. Whether those sublimits reflect the organization's actual exposure requires understanding how a specific attack scenario generates losses across those categories.

Take the example of a business email compromise leading to fraudulent payment diversion. The resulting losses can span multiple categories:

- Direct financial loss from the fraudulent transfer

- Forensic investigation to determine scope and origin

- Legal costs and potential regulatory exposure if personal data was accessed

- Notification costs where required

Quantified scenario analysis allows the CISO to estimate the probable financial impact across these categories and compare those estimates to the policy's sublimit structure. This makes it possible to determine whether coverage meaningfully transfers the financial risk or leaves the organization with more residual exposure than anticipated.

Skills That Strengthen the CISO's Contribution to Cyber Insurance Procurement

To contribute effectively to cyber insurance decisions, the CISO needs capabilities that translate cybersecurity insight into financial and risk management language that leadership, brokers, and underwriters can use.

- Quantitative risk analysis: Expressing cyber risk in financial terms through scenario modeling gives leadership a defensible basis for aligning coverage with actual exposure, rather than relying on benchmarks or prior year limits.

- Understanding policy structure: Familiarity with coverage components such as sublimits, retentions, and exclusions enables the CISO to assess whether a policy meaningfully addresses the organization’s real risk profile.

- Financial communication: Presenting cyber risk in business and financial language allows the CFO, board, and brokers to make clearer decisions about risk transfer, retention, and coverage levels.

- Awareness of underwriting expectations: Knowing which controls underwriters evaluate (such as MFA coverage, EDR deployment, patch management, and tested incident response plans) helps the organization prepare strong submissions and secure better policy terms.

Cyber Risk in the Context of Enterprise Risk Management

Putting Cyber on the Same Footing as Other Business Risks

Operational, credit, and market risks are quantified, reported, and managed against defined risk appetites. Boards and CFOs evaluate enterprise risks in financial terms. When cyber risk is presented only through qualitative heat maps or risk scores, it cannot support decisions at the same level as other enterprise risks.

A financial, quantitative view of cyber exposure allows internal and external decision makers to see trends and make better comparisons. The CISO can assess and communicate how much an incident could cost the organization, across which loss categories, and with what probability.

Industry statistics highlight the scale of cyber losses. IBM's 2024 Cost of a Data Breach report estimates the global average breach cost at $4.9 million. However, averages cannot determine the financial exposure of a specific organization or whether a policy’s coverage limits reflect its actual risk profile.

From Loss Scenarios to Coverage Structure

A CISO who takes a quantified view of cyber risk can answer critical insurance questions in a defensible way:

- Aggregate limit: Does the total policy limit reflect probable maximum loss across the organization’s top scenarios, including the possibility of multiple events in a single policy period?

- Sublimits: Are caps on specific loss types proportionate to the modeled cyber risk in those categories?

- Retention levels: Is the retention calibrated to a loss level the organization can absorb without material impact?

- Exclusions: Do policy exclusions carve out scenarios that represent significant financial risk for the organization?

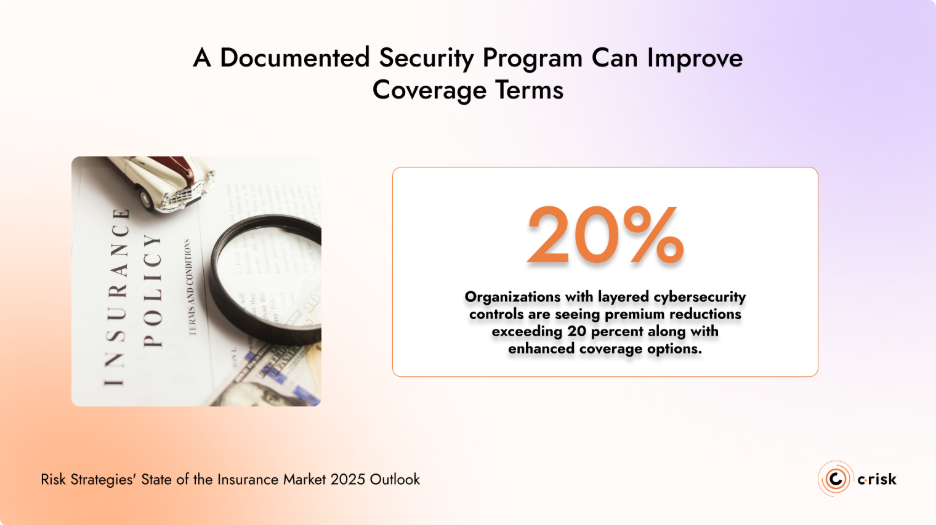

A Documented Security Program Can Improve Coverage Terms

For large enterprises where premiums run into millions of dollars, objective analysis of the organization's cyber risk profile has direct financial value. Controls performance metrics, incident response testing records, vulnerability management data, and quantified loss exposure can all contribute to better coverage terms.

According to Risk Strategies' State of the Insurance Market 2025 Outlook, organizations with layered cybersecurity controls are seeing premium reductions exceeding 20 percent along with enhanced coverage options.

Effective Risk Transfer Requires the CISO's Input

Underwriters are trying to assess the same factors the CISO already measures: how likely a loss event is, how severe it could be, and whether the organization can contain it. That overlap is not coincidental. It is the reason the CISO belongs in the insurance conversation from the outset, not as a technical resource brought in to complete forms, but as the person best positioned to translate the organization's security posture into the financial language that drives coverage decisions.

The CISO understands which systems represent the most critical exposure, which threat scenarios carry the highest probable loss, and where controls meaningfully reduce frequency and magnitude. When expressed in quantified financial terms, this knowledge provides brokers, CFOs, and underwriters with the inputs needed to structure a policy that reflects actual risk rather than sector averages.

When the CISO participates actively in the insurance process, coverage decisions improve. Sublimits can be tested against real scenarios. Retentions can be calibrated to what the organization can absorb. Exclusions can be evaluated against the threats that matter most. At renewal, the organization arrives with evidence rather than assumptions.

Cyber insurance works best when risk transfer decisions are based on measurable exposure rather than assumptions or industry averages. The CISO is uniquely positioned to provide that analysis and ensure that coverage decisions reflect the organization's real financial risk.

Work with C-Risk to Quantify Your Cyber Exposure

C-Risk works with CISOs and risk leaders to build the financial view of cyber risk that makes insurance decisions defensible. Using the FAIR methodology, we model your top loss scenarios in financial terms, map that exposure to your policy structure, and identify where coverage aligns with your risk profile and where gaps remain.